Monte Carlo Statistics — CLT and Distribution Convergence

Experience Monte Carlo methods: estimate π with random dart throwing, explore the Central Limit Theorem, perform numerical integration, and simulate random walk diffusion in real time.

Select Demo

Sample Count

Animation Speed

ms

Population Distribution

Sample Size n

Number of Trials

Integrand Function

Sample Count N

Dimension

Number of Steps

Walkers (1D mode)

Results

Estimate

—

True Value

—

Error

—

Samples N

0

Main

Convergence Chart

Visualization

Theory & Key Formulas

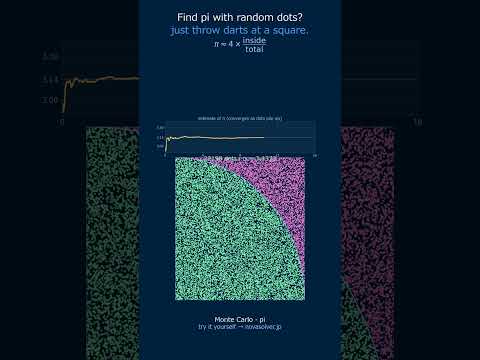

Throw random darts at a unit square. Count hits inside the quarter circle \(x^2+y^2 \le 1\):

$$\pi \approx 4 \times \frac{\text{hits}}{N}$$

Error decreases as \(O(1/\sqrt{N})\).

For population mean \(\mu\) and variance \(\sigma^2\):

$$\bar{X}_n \xrightarrow{d}N\!\left(\mu,\frac{\sigma^2}{n}\right)$$

The distribution of sample means approaches normal regardless of the original distribution.

Randomly sample \(x_i \in [0,1]\):

$$\int_0^1 f(x)\,dx \approx \frac{1}{N}\sum_{i=1}^N f(x_i)$$

Green points lie below the curve; red above.

Each step chooses a random direction independently.

Mean squared displacement: \(\langle r^2 \rangle = N(\Delta x)^2\)

This is the basis of diffusion: \(\langle r^2 \rangle = 2dDt\)

What is Monte Carlo Simulation?

🙋

What exactly is a Monte Carlo method? It sounds like a casino game, not a math tool.

🎓

Basically, it's a way to solve complex problems using randomness and statistics. Instead of a direct calculation, you run thousands of random "experiments" on a computer and average the results. For instance, to estimate the value of π, you can simulate throwing darts randomly at a square target and count how many land inside a circle drawn inside it. Try moving the "Dots per frame" slider in the simulator to see these random throws in action.

🙋

Wait, really? Throwing darts gives you π? How does that work, and is it even accurate?

🎓

It works because the probability of a dart landing in the quarter-circle is proportional to its area. The accuracy depends entirely on how many darts you throw. The error decreases slowly, following a "one over square root of N" rule. In practice, if you set the "N (upper limit)" parameter to 10,000, you might get π ≈ 3.14. Set it to 1,000,000, and you'll get closer to 3.1416. The simulator shows this convergence live.

🙋

So it's just for estimating π? What about the "Central Limit Theorem" part of the simulator?

🎓

Great question! Estimating π is just a classic demo. The real power is for problems with no easy formula. The Central Limit Theorem (CLT) is the statistical heart of why this works. It says that if you take many sample averages (like our π estimates), their distribution will always form a bell curve. In the simulator, try the CLT tab. Increase the "Repetitions" to see the histogram of sample means become a perfect normal distribution, no matter what the original random process looks like.

Physical Model & Key Equations

The core of the π estimation is a geometric probability problem. The area of a quarter circle of radius 1 is π/4. The area of the unit square containing it is 1. The ratio of hits inside the circle to total throws approximates this area ratio.

$$

\pi \approx 4 \times \frac{\text{hits}}{N}$$

Here, N is the total number of random points (darts) thrown, and hits is the count where \(x^2 + y^2 \le 1\). The statistical error in this estimate scales as \(O(1/\sqrt{N})\).

The Central Limit Theorem (CLT) provides the theoretical foundation for the reliability of Monte Carlo methods. It states that the distribution of the sample mean will approach a normal distribution as the sample size grows.

Here, \(\bar{X}_n\) is the sample mean, \(\mu\) and \(\sigma^2\) are the true population mean and variance, and n is the sample size per estimate. This means even from a non-normal process (like our dart throws), the average result over many runs is predictable and normally distributed.

Frequently Asked Questions

Increasing the number of samples N reduces the error at a rate of O(1/√N). Specifically, quadrupling N reduces the error by approximately half. Additionally, since accuracy also depends on the quality of random number generation, fixing the random seed to ensure reproducibility can be effective when necessary.

The Monte Carlo method is based on random sampling, so the estimated value fluctuates with each execution. This is a statistical error, and the smaller the number of samples N, the larger the variation. Increasing N brings the estimate closer to the true value of π and reduces the variation.

The integral of any function f(x, y) defined within the unit square can be approximated. For example, continuous functions like f(x, y) = x^2 + y^2, as well as discontinuous functions, can be handled. However, if the range of the function values is large, convergence slows down, so setting an appropriate sampling range is recommended.

If the type of original distribution used for calculating the sample mean or the sample size per trial is small, convergence slows down. Increasing the sample size (e.g., to 30 or more) and increasing the number of repetitions (number of simulations) allows a clearer normal distribution to be observed.

Real-World Applications

Financial Risk Analysis (Value at Risk): Banks use Monte Carlo to model millions of possible future market scenarios to estimate potential portfolio losses. Instead of a single prediction, they get a probability distribution of outcomes, which is far more robust for managing risk.

Engineering & Physics (Particle Transport): Simulating the path of neutrons through a nuclear reactor shield is incredibly complex. Monte Carlo methods track individual particles through random collisions, averaging the results to predict radiation shielding effectiveness and reactor criticality.

Computer Graphics (Global Illumination): To create photorealistic images, renderers like those in Pixar films use Monte Carlo path tracing. They send random rays of light from the camera, bouncing around the scene, to accurately simulate complex lighting, soft shadows, and reflections.

Project Management & Scheduling: For large projects, task durations are uncertain. Monte Carlo simulation runs thousands of trials with random task times to generate a probability distribution for the total project completion date, helping managers understand and mitigate schedule risk.

Common Misconceptions and Points to Note

First, you should avoid the overconfidence that "because it's random, it can do anything." The Monte Carlo method is not a panacea; for some problems, convergence can be painfully slow, making it impractical. For instance, if you try to directly estimate the probability of an extremely rare event (a "tail risk" in risk management), almost no points will hit the target, incurring enormous computational cost. In such cases, you need advanced techniques like importance sampling.

Next, do not underestimate the quality of "pseudo-random numbers." What simulation tools use is not true randomness but "pseudo-random numbers" generated by algorithms. In practice, if this sequence has a short period or bias, it can distort your results. For example, large-scale financial simulations require high-quality generators like the Mersenne Twister.

Finally, do not judge convergence based solely on the visual appearance of a graph. Even if the estimated value of pi approaches 3.14, that's just the result of a single run. To truly evaluate accuracy, you need to run the simulation multiple times independently (e.g., 100 times) under the same conditions and examine the variation (standard deviation) of the estimates. If you reset and run this tool with "N=10000" many times, you'll see it converges to a slightly different value each time. This is the reality of statistical error.

Select your simulation mode: Pi Estimation uses random sampling in a unit circle (set piN samples, piSpeed controls animation refresh), CLT Demonstration generates repeated sample means from a specified distribution (configure cltN sample size and cltTrial number of trials)

Adjust the input field or the sliders to modify sample counts; increase piSpeed or observe cltTrial iterations to visualize convergence toward theoretical values

Monitor histogram and statistics output: Pi Estimation converges toward 3.14159 as samples increase; CLT Demonstration shows sample mean distribution approaching normal distribution regardless of source population shape

Worked Example

For Pi Estimation: Set piN=10000 samples uniformly distributed in a 2×2 square containing a unit circle (radius=1). Expected points inside circle ≈ 7854; Pi estimate = 4×(inside/total) ≈ 3.142. With piN=50000, standard error drops to approximately 0.009, yielding estimate within 0.01 of true value 3.14159. For CLT: Draw cltN=30 observations from exponential distribution (λ=0.5) across cltTrial=500 trials; sample mean distribution shifts from skewed to approximately normal with μ=2.0, σ≈0.365.

Practical Notes

Convergence rate follows O(1/√N): doubling samples reduces error by ~29%; use piSpeed=fast for N>100000 to avoid lag while observing asymptotic behavior

CLT robustness increases with cltN—highly skewed distributions (Poisson λ=1) need cltN≥50 for visible normality; cltTrial≥300 stabilizes histogram shape

Integration via Monte Carlo: volume estimates for complex geometries require proportionally larger sample counts than simple circle; systematic bias appears when cltN<5

🎬 Watch it in motion

Monte Carlo | a rain of random dots pins down pi #Shorts